Economy part 2: What everything actually costs

Demographic collapse of Czech republic part 3

In the last article we touched on the price of two incomes in a family and how, in reality, it makes very little tangible difference in that family wealth build up due to scarcity inflated prices of inelastic goods. Now this can be understood as poor legislation and slow grinding wheels of any bureaucracy. Which is not great, but at least understandable. What’s why in this article, we’ll cover the slightly more instinctively unjust aspects. yay.

The Czech Republic is a net exporter of electricity. In fact we export about 25-30% consistently. The surplus goes mostly to economies connected with ours, such as Germany, Austria, Slovakia and so on. Czech people are aware of it, and quite proud I’d say, because it’s one of the things we’re good at and supports our growing economy without relying on imports too much. It makes us look strong and independent. What is less advertised is that Czech households pay among the highest electricity prices relative to wages in the European Union. Now that’s a little odd right?

The mechanism is a “feature” of EU energy market design, not a bug, or at least not a bug anyone with power has been motivated to fix. The wholesale electricity price across the interconnected European market is set by the most expensive generator required to meet demand at any given moment. That generator is almost always gas. So the price of Czech electricity, generated substantially by nuclear and coal plants that cost a fraction of gas to run, is set by the gas price. That same gas that got one of the biggest shipping pipelines blown up during the Ukraine conflict and by that became even more expensive. So Czech nuclear output is sold at gas prices. The spread between what it costs to generate and what the household pays does not disappear. It goes to generators and to the cross-border trading structures that sit between production and consumption.

During the German gas crisis of 2022 the full absurdity of this became visible. Czech households paid the German emergency price for electricity that had nothing to do with German gas. The state intervened with subsidies, which is to say it borrowed money to pay the spread that the market design was extracting from its citizens. The underlying design was not changed. And then the subsidy ended, you can imagine how well that went. So not only did we increase our national debt to finance nonsense, but of course the prices remained elevated relative to wages. And the Czech household filed it under the general category of things that are expensive now and moved on. Mainly because we don’t have a choice. Doesn’t mean we’re not upset. I think if people knew as much as I had to research into this, there’s a distinct possibility of heads on spikes or more likely, couple revivals of the old defenestration tradition.

I’m starting with electricity because it’s one of the starker ones and in people’s subconscious as a fact about our country, but it is the same pattern that appears in housing, in food, and in the tax structure. Naming it explicitly, such as I will do here, is the first step toward shifting in the right direction. The state, or a structure above the state, creates conditions that systematically transfer value away from households and toward capital or institutional interests. Then the state responds to the resulting distress with targeted interventions that treat the symptom without touching the mechanism. Maybe borrow some extra to patch it over, increase state debt and tax the citizen that much more because of course we have to deal with our debt collectively. We share in the responsibility, but not the rewards. And the mechanism continues.

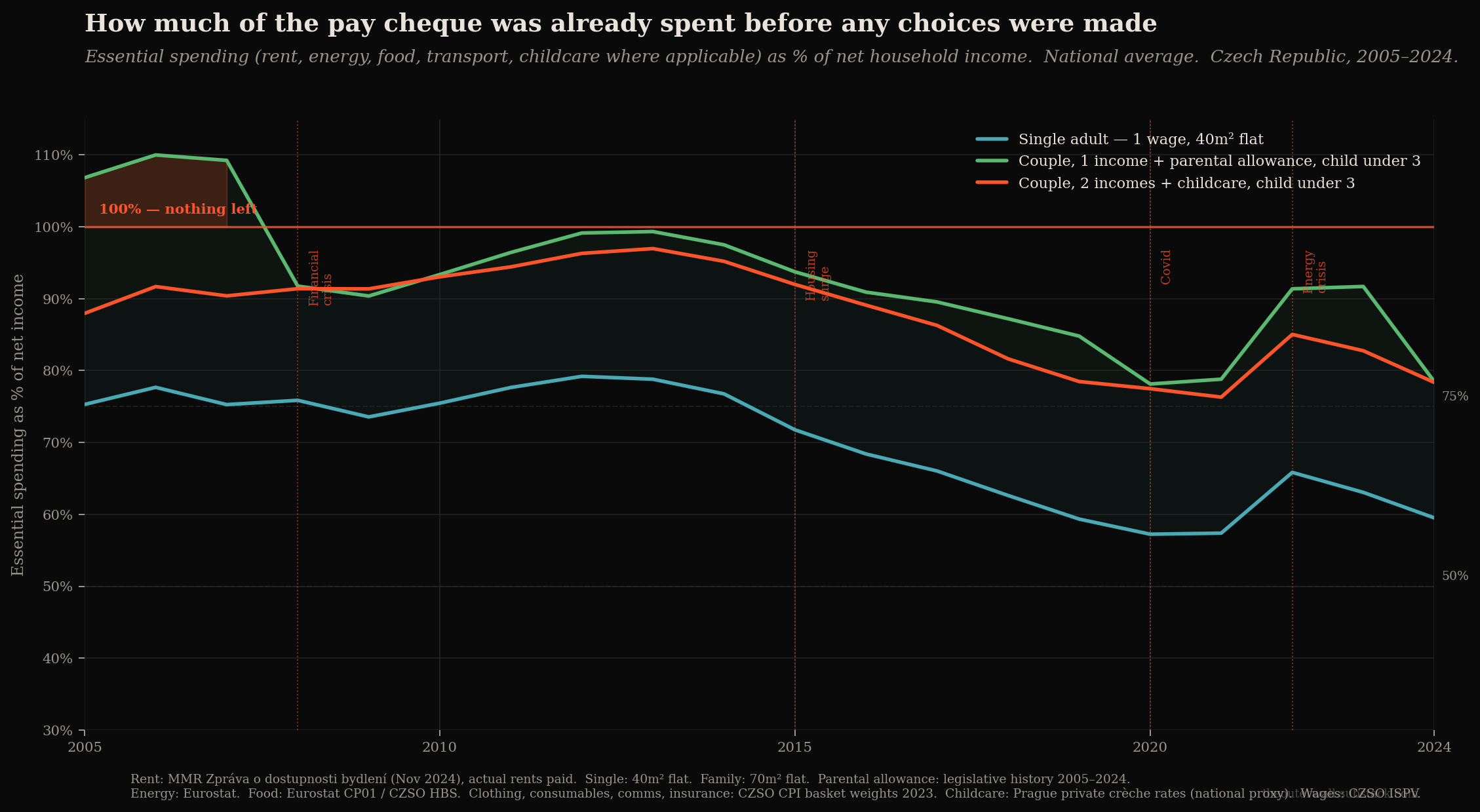

Here you can see the rough graphing out of that essential spending for individuals and families, relative to their salary. So how much we realistically have left after we pay for everything necessary to function in our society. The chart models three household types on national average figures for the Czech Republic between 2005 and 2024. The essential spending basket includes rent (based on average rents actually paid across existing tenancies, sourced from the Ministry for Regional Development's 2024 housing report. Not portal asking prices, which run substantially higher so new entries into the market will be much worse off), electricity, gas and water at Eurostat retail prices, food at the Czech Statistical Office household budget survey baseline indexed through food CPI, transport modelled as 70 litres of fuel per month for the single adult and one-income family, clothing and footwear, household consumables including toiletries, cleaning products and nappies for the family scenarios, communication costs covering phones and internet, and basic car insurance. For the two-income scenario, childcare is included at Prague private daycare rates used as a national proxy, and the parental allowance is removed as it ceases when both parents return to work. For the one-income scenario, the parental allowance is modelled through all legislative changes from 2005 to 2024, including the 2008 reform and the 2024 increase to 14,600 CZK per month, though that 2024 figure should be read as a policy change rather than an improvement in underlying household economics, since the pool is finite and the mechanism that makes the second income unattractive remains intact. What the basket does not include: mortgage costs, healthcare co-payments and dental, school costs, car maintenance and STK inspection (which average roughly 600-800 CZK per month over a typical ownership cycle), home contents insurance, savings, or any discretionary spending. The figures reflect national averages throughout; households in Prague and Brno face substantially higher rent and childcare costs against the same median wage, and the picture there is correspondingly grimmer.

The unavoidable costs

Since we have discussed low supply in the housing market with insane demand, now it’s time to have a look at the items that don’t suffer from long term planning as much, but the costs keep climbing for … reasons. Energy is not the only item in the basket of things Czech families cannot opt out of. It is just the most illustrative, because the paradox is so clean. Here is the rest of it.

Food. The Czech Republic is (only) between 30 and 40 percent self-sufficient in its total food basket despite having significant agricultural land and a functioning farming sector. This makes sense, almost no country can produce the variety we got used to through global market flow. We can’t reliably grow oranges, we grow wheat and rear cows. The retail market is 59 percent controlled by three foreign-owned chains, the Schwarz Group, the Rewe Group, and Ahold due to competetive pricing. Czech farmers grow the crop. Czech processors transform it into yummy not raw stuff. Foreign chains set the shelf price and capture the margin. Czech processors are squeezed from both ends, paying European input prices for energy, fertiliser and packaging, while selling to buyers who can replace them with Polish or German product if the terms become inconvenient. The value capture happens at the retail end. The retail end is not Czech-owned. Higher quality but less affordable Czech products are often left on the shelves. This is the inverse of what you might expect: Czech consumers are in some respects being priced away from Czech-produced food in favour of cheaper imports selected by foreign-owned chains optimising for margin. The reality is that Czech agricultural production and Czech retail consumption are largely disconnected from each other, and the chain between them is where the value disappears. And you won’t believe who pays the difference.

This is not necessarily an argument for protectionism or for restricting foreign investment. It is a structural observation about where the pricing power sits, and therefore where the benefit of any increase in household food expenditure goes. When Czech food prices rose sharply in 2022 and 2023, the profits of the major retail chains rose with them. Margin compression in a crisis is not what the data showed. The Czech household absorbed the increase. The chains reported strong results.

Housing and mortgage servicing: This was covered in the previous article, but the rate dimension deserves a specific mention here. The Czech National Bank’s benchmark rate peaked near 7 percent in 2022 and 2023. Households that had fixed their mortgages in 2019 or 2020 at under 2 percent faced refixing at triple or quadruple that rate on assets whose prices had not fallen to compensate for the higher cost of debt. The monthly payment on a Prague apartment did not adjust to reflect the new rate environment. The asset price held, because supply remained constrained. The household absorbed the difference. This one was quite a shock that I saw play out multiple times in my circles. Friends who were quite comfortable (not wanting for anything and saving), suddenly found themselves barely getting by or running negative monthly budgets.

Healthcare: The Czech public system is, by most objective measures, genuinely good. It ranks fourteenth in Europe, delivers broad coverage at relatively low per-capita cost, and for acute care it compares favourably with systems that spend substantially more. The doctors are competent, the infrastructure works in most cases. Or put it this way, I experienced much worse when I was living in other countries. The actual problem is not quality, it is what the system costs the household in aggregate, and what it prevents the household from doing with that money instead.

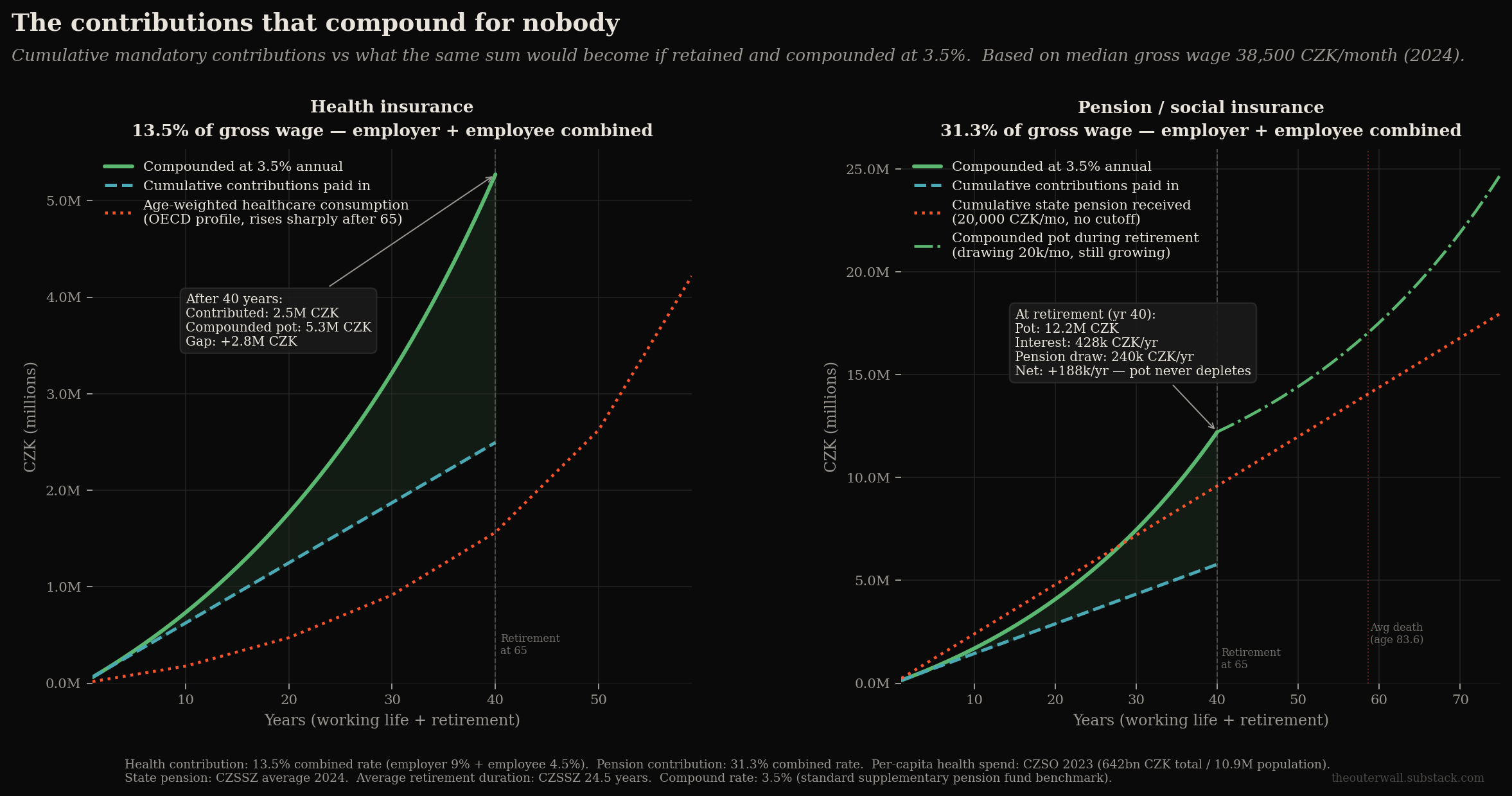

The combined health insurance contribution is 13.5% of gross salary, split between employer and employee. On a median wage that is around 5,200 CZK (213.42 EUR) per month, or roughly 62,000 CZK (2,544.6 EUR) per year, leaving the household entirely. The system spends 59,000 CZK (2,421.48 EUR) per person per year across the entire population of newborns, pensioners, the chronically ill, everyone. Even if you assumed a working-age adult consumed the full population average every single year for forty years, the total would be 2.36 million CZK (96,859.12 EUR) . But 62,000 CZK per year invested at a modest 3.5% (the kind of rate a standard supplementary pension fund compounds at) grows to approximately 5.3 million CZK (217,522.60 EUR) over those same forty years. The compounded pot would be nearly double the total spend, before you even start drawing on it for the genuinely expensive final years. The healthy working-age contributor is not just paying for their own care. They are net funders of the system during the precise decades when retained and compounded money would be worth the most. By the time they become net consumers of what they paid in, four decades of potential compounding will simply not have happened. So this turns into an argument about opportunity cost. The contributions were spent in the year they were collected, and the opportunity cost accumulated silently in the background, visible only as the gap between what the household owns and what it might have.

There is a version of this that a smarter state could run differently. A sovereign health fund that accumulates during working years and draws down in old age, aligning contribution with consumption across a lifetime rather than running a permanent transfer from the young to the current sick. There is also a version where individuals manage it themselves, with appropriate catastrophic cover retained as genuine insurance and choice of provider, driving competition is a state funded system. No one researches harder than when their own health and money are at stake simultaneously. Instead, the household has no ability to redirect the contribution, no mechanism to compound the difference, and no transparency about what proportion of what they pay represents genuine risk pooling versus a structural transfer they were never asked to consent to.

The catastrophic risk case is real. A serious diagnosis at forty-five, a premature birth, a major accident,etc. These can consume years of contributions in weeks, and pooling that risk across a population is the legitimate function of insurance. But there is a difference between pooling genuine catastrophic risk and collecting a contribution sized for a system under severe demographic pressure and handing back something sized for a healthy young family. The household cannot distinguish between the two, cannot opt out of the transfer component, and is left to simply absorb the cost alongside everything else.

On top of the compulsory contribution sits a private layer that the public system’s structural constraints have made near-mandatory in practice. Not because the public system is incompetent, but because it is stretched enough that timeliness has become a commodity. The private layer sells queue bypass, not necessarily superior medicine. Dental treatment sits almost entirely outside public insurance regardless. Pregnancy has accumulated a standard budget line of supplementation and monitoring products that previous generations did not carry, partly because the products did not exist and partly because the medicalisation of normal life stages has created expenditures that feel optional but are not, in the specific sense that declining them carries a social cost as well as a practical one.

Pension: This is always a big one, but thankfully for me, it functions in much the same way healthcare does. Well thankfully only in saving me writing time but little else. Social insurance compounds the same problem at nearly twice the scale. The combined contribution of employer and employee together is 31.3% of gross salary against health insurance’s 13.5%. On a median wage that is roughly 12,000 CZK (492.50 EUR) per month, 144,000 CZK (5,910.05 EUR) per year, leaving the household with the same finality and the same destination: spent immediately on current obligations, accumulated nowhere, compounding for nobody. The system is pay-as-you-go by design, which was a reasonable architecture when six workers supported one pensioner. It is a rather different proposition at 1.7 to one, which is where our sons and daughters enter the workforce.

Apply the same arithmetic. 144,000 CZK per year at 3.5% over 40 working years compounds to approximately 12.2 million CZK (500,712.40 EUR). The state pension a median earner can currently expect is around 20,000 CZK (820.84 EUR) per month. Once the pot reaches that level at retirement, it generates roughly 428,000 CZK (17,565.98 EUR) per year in interest. The state pension draws 240,000 CZK (9,850.08 EUR) per year. The pot grows by around 188,000 CZK (7,715.90 EUR) net every year, in perpetuity, without any further contributions ever (in theory, and assuming the fund achieves 3.5% growth steadily, which over long periods is not unrealistic). Instead, the contributor receives a document confirming how long they participated. Not how much they paid.

To illustrate my point in practical terms: the compounded pot from social contributions alone, roughly 12.2 million CZK at retirement, would fund the contributor's own pension at current rates for the full average retirement span of 24.5 years and still leave approximately 4.6 million CZK (188,793.20 EUR) in surplus. Enough to fund roughly 80% of another person's retirement entirely. The pay-as-you-go architecture did not just transfer money from young to old. It forfeited the compounding that would have made the demographic cliff survivable. A funded system accumulating over forty years would have built the buffer the country now desperately needs. Instead it was spent in the year it was collected, every year, for decades, and now the cliff is here and the buffer does not exist.

Car: Outside Prague and Brno, and in significant parts of those cities too, public transport geography makes private car ownership functionally non-optional, not a lifestyle preference. It is a consequence of how Czech towns and suburbs are built, how employment is distributed, and how the transport infrastructure has been developed and neglected over decades. Because from my house to work, it’s either hour and half on a train, or 35 minutes by car. I do not want to spend less time away from my family.. The cost of that non-optional car, insurance, fuel, mandatory technical inspections, motorway vignette, has risen consistently and compounds into a fixed household outgoing that absorbs a significant share of income before any discretionary spending begins.

The tax wedge

The state is not a passive observer of this list. It has its own line in the household budget, and that line has been moving in one direction.

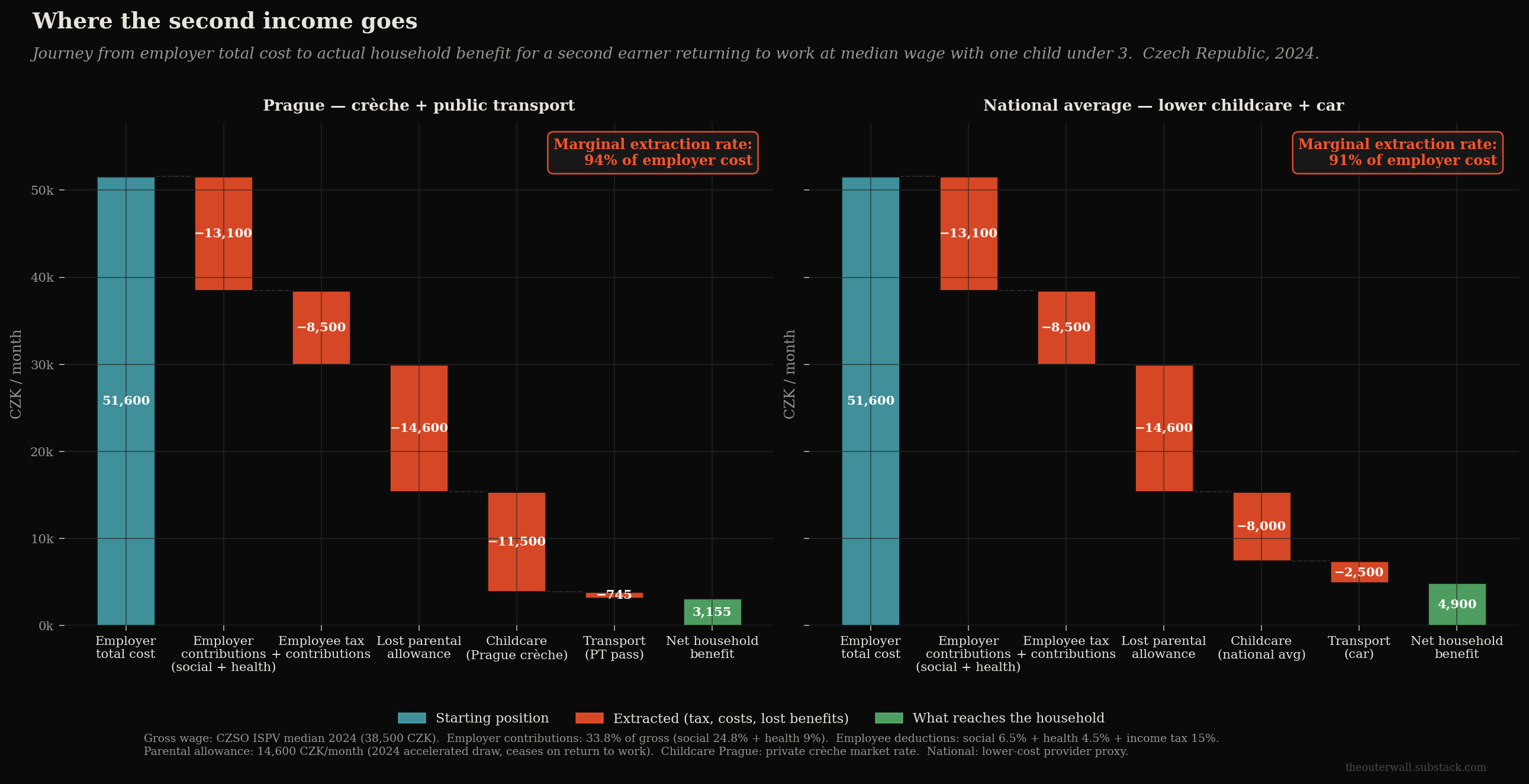

The effective tax burden on Czech labour, measured through the OECD’s taxing wages methodology, has increased. The specific configuration that produces the sharpest number is the one most relevant to this series: the marginal effective rate on the second income in a household with young children, once childcare costs are treated as a function of that income, approaches or exceeds the gross wage in the lower income bands. The state simultaneously needs the second earner in the workforce to fund pension and social spending. It then taxes that second earner at a rate that makes the financial case for working questionable. This is not a paradox. It is a design feature of a fiscal system that requires broad labour participation to sustain transfer payments, regardless of whether that participation makes sense for individual households.

Czech state debt requires continuous rollover (and ours is relatively mild in comparison to European countries (43.6% of GDP vs. average of 80.7%). The fiscal constraints this creates have historically been resolved through increases in labour taxation rather than capital or property taxation, because labour income is visible, traceable, and easy to administer. Capital gains, property wealth, and retained earnings in corporate structures are considerably harder to tax and are represented by constituencies with considerably more political leverage than households with young children and high housing costs. The people least able to absorb additional taxation are taxed at the highest marginal rates relative to their actual capacity. This is not conspiracy. It is the path of least administrative resistance, followed consistently.

The one that worked

It would be dishonest to present this as a story in which nothing ever works, because one sector tells an upliftingly different story.

Mobile and internet services in the Czech Republic have fallen in real price over the same period that housing, energy, food, and transport were rising. Coverage is good. Prices are competitive by European standards. The explanation is straightforward: the market was genuinely competitive, with multiple operators unable to coordinate pricing or restrict entry, and the result was that consumers captured the benefit of technological improvement rather than having it absorbed by concentrated market power or institutional bottlenecks. Or interfering government.

Despite being a relatively minor spending (most likely due to lack of exploitable mechanisms), it sets the structural argument in one example. Where competition was real, prices fell and quality improved. Where it was absent, captured, or deliberately designed otherwise, the opposite happened. The question for housing, for energy, for food retail, is not whether market mechanisms work. It is whether the specific market in question is structured to make them work, or structured to prevent them from doing so. In each case where Czech household costs have risen beyond what wages can absorb, you will find the same answer: a market whose structure was set by institutional or regulatory choices, not by natural scarcity or genuine supply constraints.

The pattern

There is a thread running through both of the economic articles that I would like to explicitly highlight.

In housing, the state’s planning and permitting system created an artificial scarcity. Private capital recognized the opportunity and entered the market, acquiring an interest in keeping that scarcity in place. The state now finds it difficult to act against the interest it created, because the capital that benefits is both economically significant and politically connected. The household pays the resulting price, and the state responds with occasional demand-side subsidies that do not alter the supply constraint.

In energy, a supranational design choice set the pricing mechanism. Czech generators benefited. Czech households paid the resulting premium. The state borrowed to cover the gap during the acute crisis, socialized the cost, and left the mechanism intact.

In food, regulatory frameworks permitted a retail consolidation that transferred pricing power out of Czech hands. The beneficiaries are incorporated elsewhere. The cost is carried by Czech households shopping at Czech supermarkets buying food grown on Czech land. This one is entirely out of the governments grasp by now, unless we can expand our industry in this sector. But there are no incentives for it.

The pattern is not that markets are bad or that the state is corrupt in any dramatic sense. The pattern is that policy choices, made at the state or supranational level, repeatedly create conditions in which value is systematically extracted from households and transferred to capital structures, and then the state responds to household distress with targeted transfers that treat the symptom and preserve the mechanism, usually by increasing national debt, therefore taxation later on. This is sustainable as long as households can absorb it. The previous article in this series made the case that one generation is approaching the limits of what it can absorb and is very worried about the next one.

The balance sheet

None of the items in this basket are catastrophic in isolation. The family budget can survive more expensive electricity, or higher mortgage rates, or food prices that rise faster than wages, or the private dentist, or the mandatory car and pricier gas because war disrupts the supply chain. What it cannot absorb indefinitely is all of them, simultaneously, rising faster than income, for twenty years, while the tax burden climbs and the informal support structures that once distributed the cost of family life have been dismantled and replaced by market services that charge for what grandmothers used to do for free.

Headline inflation captures some of this, but only the part that moves. It measures price changes in a fixed basket of goods and largely misses the structural layer underneath. The energy bill priced at the European marginal rate regardless of whether the country is a net exporter, the food bought from a foreign-owned chain at processed-goods prices on an Eastern European wage, the deposit that the planning system has made structurally unreachable, the health contribution sized for a demographically ageing population rather than the healthy young family paying it, the pension contribution that will be spent in the year it is collected and compound for nobody. These are not price spikes. They are permanent features of how the household is positioned relative to the systems it cannot opt out of. Inflation falls back. These do not.

Each item is individually defensible. The energy pricing mechanism has a logic. The retail concentration has a logic. The pay-as-you-go pension has a logic. The planning system has a logic. The sum of them is what the charts aim show, because no single inflation figure will ever tell you.

The demographic article in this series identified the Czech family formation crisis as the central long-term threat to civilisational continuity. This one has tried to show that the crisis is not a values failure alone, or a cultural drift, or a generation too selfish to have children. It is also a balance sheet problem. And the balance sheet has been deteriorating systematically, through specific mechanisms, by identifiable policy choices, for long enough that the generation now of childbearing age has never known it to be otherwise.

That generation is not failing to have children because it does not understand the importance of the next generation. It is looking at the numbers, running the arithmetic honestly, and arriving at a conclusion that the numbers support. The question is not how to persuade them otherwise. It is whether anyone in a position to alter the numbers is willing to do so.

That is a political question, which means it is also, ultimately, yours to answer.

The next article, and hopefully last in this mini series, because I am absolutely spent and borderline depressed from going down this particular rabbit hole, will try to name what changing them would actually require.